| Period | Type | Revenue | Profit* | Margin |

|---|---|---|---|---|

| 1999/9 | Non-consol. Revenue / Net Income | ¥0B | - | - |

| 2000/9 | Non-consol. Revenue / Net Income | ¥3B | - | - |

| 2001/9 | Consolidated Revenue / Net Income | ¥6B | -¥2B | -32.4% |

| 2002/9 | Consolidated Revenue / Net Income | ¥11B | -¥0B | -2.7% |

| 2003/9 | Consolidated Revenue / Net Income | ¥16B | -¥2B | -14.9% |

| 2004/9 | Consolidated Revenue / Net Income | ¥27B | ¥4B | 15.0% |

| 2005/9 | Consolidated Revenue / Net Income | ¥43B | ¥2B | 5.7% |

| 2006/9 | Consolidated Revenue / Net Income | ¥60B | ¥4B | 7.1% |

| 2007/9 | Consolidated Revenue / Net Income | ¥76B | ¥2B | 2.6% |

| 2008/9 | Consolidated Revenue / Net Income | ¥87B | ¥1B | 1.1% |

| 2009/9 | Consolidated Revenue / Net Income | ¥94B | ¥1B | 1.3% |

| 2010/9 | Consolidated Revenue / Net Income | ¥97B | ¥5B | 5.6% |

| 2011/9 | Consolidated Revenue / Net Income | ¥120B | ¥7B | 6.1% |

| 2012/9 | Consolidated Revenue / Net Income | ¥141B | ¥9B | 6.0% |

| 2013/9 | Consolidated Revenue / Net Income | ¥162B | ¥11B | 6.5% |

| 2014/9 | Consolidated Revenue / Net Income | ¥205B | ¥10B | 4.6% |

| 2015/9 | Consolidated Revenue / Net Income | ¥254B | ¥15B | 5.8% |

| 2016/9 | Consolidated Revenue / Net Income | ¥311B | ¥14B | 4.3% |

| 2017/9 | Consolidated Revenue / Net Income | ¥371B | ¥4B | 1.0% |

| 2018/9 | Consolidated Revenue / Net Income | ¥420B | ¥5B | 1.1% |

| 2019/9 | Consolidated Revenue / Net Income | ¥454B | ¥2B | 0.3% |

| 2020/9 | Consolidated Revenue / Net Income | ¥479B | ¥7B | 1.3% |

| 2021/9 | Consolidated Revenue / Net Income | ¥666B | ¥42B | 6.2% |

| 2022/9 | Consolidated Revenue / Net Income | ¥711B | ¥24B | 3.4% |

| 2023/9 | Consolidated Revenue / Net Income | ¥720B | ¥5B | 0.7% |

| 2024/9 | Consolidated Revenue / Net Income | ¥803B | ¥16B | 2.0% |

Author's Insights

In March 2000, CyberAgent went public on the TSE Mothers market while still in the red, raising 20.7 billion yen. The valuation of 62.4 billion yen was dependent on expectations of future growth, and the disconnect from business reality was evident. At the time, stock valuations were based not on earnings but on price-to-sales ratios, and growth expectations themselves were priced in. Immediately afterward, the dot-com bubble burst, and the market capitalization plunged to around 10 billion yen. An abnormal situation arose in which cash on hand exceeded the company's enterprise value, and demands for cash distribution from the Murakami Fund, among others, turned the "over-raised capital" itself temporarily into an existential management risk. Many companies benefited from the bubble during this period, but how they used those funds determined entirely different trajectories thereafter.

A symbolic contrast is On the Edgj (later Livedoor), the very company to which CyberAgent outsourced the development of CyberClick. Livedoor, led by Takafumi Horie, also went public during the same period and positioned stock-swap-based corporate acquisitions—leveraging its high stock price—as the axis of its growth strategy. The model treated maintaining a high stock price as having intrinsic value as acquisition currency, designing a system that used shares themselves as a management resource rather than deploying funds into business operations. Susumu Fujita, on the other hand, chose to preserve the raised cash and use it over the long term as a source of business investment. Whether to use bubble-acquired capital for "maintaining the stock price" or for "deploying into business"—this fork decisively separated the two companies' subsequent paths.

CyberAgent's 20.7 billion yen continued to function as the source of large-scale investment for the ensuing 20 years. Approximately 6 billion yen was invested upfront in the Ameba business from 2005, with Fujita personally overseeing the business and spending five years to bring it to profitability. In AbemaTV, established in 2015, cumulative investment on the order of hundreds of billions of yen was made, and even while carrying 111.1 billion yen in negative equity, the company continued investing from its own funds without relying on external financing. It refused the Murakami Fund's demands for capital return, and when GMO expanded its shareholding, CyberAgent defended its management through an alliance with Rakuten, maintaining the capacity to "bet big someday" without succumbing to short-term shareholder return pressure. Without these defensive and preservation decisions, the subsequent large-scale investments would not have been possible.

No few companies squandered funds raised during the bubble. There were numerous examples during the same period of companies sitting on excess cash and failing through purposeless diversification or M&A. Livedoor's stock-price-linked growth model collapsed with the 2006 scandal, and the company itself ceased to exist. In CyberAgent's case, the sheer size of the capital raised was a product of the era, but gradually converting it into business investment over 20 years was the result of management decisions. Despite benefiting from the same bubble, the difference in how capital was used determined the lifespan of each company. This contrast suggests the principle that the quality of capital raising is determined not at the point of raising but by how the capital is subsequently used.

Since its launch in 2016, AbemaTV has incurred annual costs of hundreds of billions of yen for program production and content procurement, and by 2022 had fallen into negative equity of 111.1 billion yen. Viewed in isolation, this is clearly an unsustainable financial state, and under normal circumstances would compel either external fundraising or business withdrawal. When Susumu Fujita declared at the establishment of AbemaTV that he would "continue investing for 10 years," the underlying recognition was that this was not a business that could generate returns in the short term. Yet CyberAgent continued investing in AbemaTV from its own funds without relying on external financing. This decision cannot be explained by determination alone.

What made this possible was the design of the business portfolio on a consolidated basis. The advertising business generated stable earnings, and the gaming business posted explosive profits driven by the hit title Uma Musume. In fiscal 2021, the company achieved record-high consolidated operating profit of 104.3 billion yen, and a structure was in place that absorbed AbemaTV's losses while still maintaining high profitability. CyberAgent is often discussed as a company that mass-produces new businesses by appointing young employees as subsidiary presidents, but what actually supports consolidated earnings are a small number of businesses where large-scale investment was decided at the headquarters level: advertising, gaming, and AbemaTV. The proliferation of subsidiaries may contribute to organizational vitality and motivation, but in terms of portfolio reality, it is the big bets placed by headquarters that define the earnings structure.

This design philosophy can be read not as a single-year decision but as an accumulation of multiple decisions. Selling the FX business—which was generating 3.2 billion yen in operating profit—for 21 billion yen in 2013 and concentrating on smartphones and gaming was a swap of "earning businesses." The stabilization of the advertising business, the establishment of Cygames to launch the gaming business, and the long-term investment in AbemaTV—viewed individually these are separate decisions, but in the context of the overall portfolio, a consistent structure emerges: "continuously replacing earning businesses in line with the times while maintaining investment capacity for businesses where bets are placed." Behind the corporate image of prolific new business creation, the number of essential earnings drivers is extremely limited.

What the AbemaTV case brings to light is that the feasibility of long-term investment is determined not by strength of will but by structure. Resolve to endure losses alone does not sustain funding. The company must possess "earning businesses" that support "betting businesses" and must also be willing to reconfigure those earning businesses in response to changes in the market environment. Many companies proclaim long-term investment yet abandon it midway—perhaps not because their resolve is weak but because the earnings structure designed to support it is insufficient. It is this dynamic management of the portfolio that may have been the mechanism enabling decade-scale large-scale investment.

CyberAgent established

Zero engineers, zero proprietary products. What Susumu Fujita chose was the sales agency business for WebMoney—essentially selling someone else's product. Yet this choice was also a rational design that minimized initial investment while simultaneously acquiring customer touchpoints and market intelligence. The insight gained on the sales floor—that 'advertisers want measurable results'—led directly to the CyberClick entry just four months later. Starting without a product paradoxically increased the freedom to observe the market.

BackgroundStructural gap in the nascent internet market

In the late 1990s, the internet was beginning to spread rapidly in Japan, and numerous venture companies were being founded. However, most internet companies at the time were technology-oriented, and many lacked a well-developed sales infrastructure. There were frequent cases of companies that possessed excellent services but missed growth opportunities due to insufficient sales capabilities.

While the market was in an expansion phase, sales functions connecting technology with customers were in short supply. Small internet companies in particular found it difficult to secure sales talent, and there was demand for outsourcing sales to external parties. This structural gap was emerging as a new business opportunity.

DecisionLeft his job at age 24 to start a business

In March 1998, Susumu Fujita, then 24 years old, left the staffing company Intelligence and founded CyberAgent in Minato-ku, Tokyo. Despite his youth, he launched with a business model centered on "sales agency" work, leveraging his own sales experience.

Drawing on his track record of success in internet media sales as a new graduate, he first secured a sales agency contract for the payment processing service WebMoney. By not holding proprietary products and specializing in the sales function, he chose a strategy that minimized initial investment while riding the wave of market expansion.

ResultFoundation for advertising business development

The sales agency model rapidly expanded the customer base, establishing a certain presence within the internet industry. Through customer interactions, the company gained an understanding of the advertising market structure and formed the groundwork for identifying the next business opportunity. The founding-era experience directly led to the subsequent pivot.

The subsequent entry into cost-per-click advertising was made possible precisely because of the market understanding and relationships built through sales. The founding at age 24 became the origin of CyberAgent's growth into an advertising and media company.

Zero engineers, zero proprietary products. What Susumu Fujita chose was the sales agency business for WebMoney—essentially selling someone else's product. Yet this choice was also a rational design that minimized initial investment while simultaneously acquiring customer touchpoints and market intelligence. The insight gained on the sales floor—that 'advertisers want measurable results'—led directly to the CyberClick entry just four months later. Starting without a product paradoxically increased the freedom to observe the market.

CyberClick sales commenced

After failing to develop the ad delivery system in-house, the company fully outsourced to On the Edgj. In exchange for paying 10% of revenue as royalty, it secured a five-year exclusive contract. This contract design was shrewd. It prevented the same technology from flowing to competitors while using a clear pricing structure of 140,000–180,000 yen per 2,000 guaranteed clicks to acquire SME clients, securing 4,728 media outlets by January 2000. A suggestive case of a company without technology capturing the market through 'monopoly over the mechanism.'

BackgroundFocus on cost-per-click advertising

In 1998, the mainstream internet advertising formats in Japan were impression-based and period-based, with advertisers paying based on the number of impressions or the duration of placement. Performance measurement was limited, and the relationship between advertising spend and results was opaque. Meanwhile, in the United States, performance-based advertising that charged per click was beginning to spread, attracting attention as a rational model for advertisers.

Newly founded CyberAgent initially had WebMoney sales agency as its main business, but during its sales activities encountered ValueClick Japan's cost-per-click advertising and took on its distribution. Responses from small and medium-sized enterprises in the field were positive, and the company realized the latent demand for advertising models that could clearly demonstrate cost-effectiveness. At a juncture when internet adoption was accelerating, the market expansion potential was judged to be significant.

DecisionEntry through imitation and an exclusive contract

The company decided to go beyond sales agency work and develop cost-per-click advertising as a proprietary product. It named the product "CyberClick" and pivoted the business axis from sales agency to advertising company. However, system development—including click measurement and fraud prevention—proved more difficult than anticipated, and the initial attempt at in-house development failed.

Consequently, a contract was signed with On the Edgj (later Livedoor) fully outsourcing development and operations. The contract specified a royalty of 10% of revenue and was structured as a five-year exclusive agreement starting September 1998. This prevented technology leakage to competitors while establishing the framework for entry into the performance-based advertising market.

ResultEstablishment of the advertising agency model transition

Following system launch in October 1998, full-scale CyberClick sales commenced. Pricing was set at 140,000 to 180,000 yen for a guarantee of 2,000 clicks, with cost-effectiveness pitched by comparison to conventional direct mail costs. The primary customers were cash-strapped venture companies and SMEs, and a sales strategy distinct from traditional media was deployed.

Media acquisition progressed simultaneously, and by January 2000, 4,728 media outlets had been secured. A framework for matching advertisers and media through the system was established, and the company completed its full transition from a sales agency business to an internet advertising company. The commencement of sales in July 1998 became a symbolic turning point marking the departure from the founding business.

| Product Name | Launch Year | Listed Media Count | Cost Per Click |

| CyberClick | October 1998 | 4,728 (web) | 70–90 yen |

| ClickIncome | January 1999 | 2,536 (email) | 110–140 yen |

- Product Name

- CyberClick

- Launch Year

- October 1998

- Listed Media Count

- 4,728 (web)

- Cost Per Click

- 70–90 yen

After failing to develop the ad delivery system in-house, the company fully outsourced to On the Edgj. In exchange for paying 10% of revenue as royalty, it secured a five-year exclusive contract. This contract design was shrewd. It prevented the same technology from flowing to competitors while using a clear pricing structure of 140,000–180,000 yen per 2,000 guaranteed clicks to acquire SME clients, securing 4,728 media outlets by January 2000. A suggestive case of a company without technology capturing the market through 'monopoly over the mechanism.'

CyberAgent's flagship product is cost-per-click advertising. It charges based on the actual number of times banners or text are clicked—if 10,000 clicks are guaranteed, the ad runs until 10,000 people visit the company's website. (...)

Going forward, we intend to focus on performance-based advertising. However, performance-based advertising is a challenging business model for advertising agencies. Just because someone clicks a banner and lands on a company's website doesn't mean they'll purchase the product on the spot. Even if they decide to buy, some people may feel uneasy about purchasing online and buy at a physical store instead. It's difficult to verify the effectiveness.

Nevertheless, having advertising costs proportional to effectiveness is an ideal pricing mechanism for advertisers. Resistance to buying things on the internet is fading, and we are determined to establish this as a business.

Listed on the TSE Mothers market

A loss-making company raised 20.7 billion yen at a valuation of 62.4 billion yen, only to see its market cap crash to 10 billion yen six months later. The abnormal situation of cash holdings exceeding enterprise value invited intervention from the Murakami Fund. Yet ironically, the 20 billion yen-plus in cash raised at the bubble's peak enabled the long-term investments in Ameba and Abema that followed. The structure in which funds raised at the bubble's peak became the investment capacity for a decade-plus of loss-making businesses is fascinating.

BackgroundCapital market frenzy during the dot-com bubble

From 1999 to 2000, expectations for internet-related stocks surged rapidly in the Japanese equity market, and the Mothers market became the stage for growth company fundraising. CyberAgent was also expanding its advertising transaction volume, but the business was still in the red, and its valuation was based on the premise of future growth. At the time, stock valuations tended to be based not on earnings but on price-to-sales ratios (PSR), and growth expectations themselves were priced in.

As of September 1999, just before the listing, the valuation was approximately 150 million yen, but in just six months the valuation inflated dramatically. Overheated expectations for the internet industry created an environment that supplied massive funding to a company in only its second year of existence. Susumu Fujita determined that maximizing growth velocity required raising capital directly from the market, and chose an early listing.

DecisionExecuted a large-scale IPO while still in the red

In March 2000, the company achieved listing on the TSE Mothers market, raising 20.7 billion yen based on a valuation of 62.4 billion yen. With virtually zero interest-bearing debt, the company established a strong financial position with approximately 20 billion yen in net cash immediately after listing. Attracting attention as the youngest CEO to take a company public at the time, the company became a symbolic figure of the dot-com bubble.

However, the business was still in the red, and the valuation depended on future expectations. The use of funds was not clearly defined, and the company embarked on expansion-oriented management, including relocating headquarters to Shibuya Mark City. The decision to raise capital on the premise of growth was a bold choice that could only have been viable in a bubble environment.

ResultCapital surplus and divergence from market valuation

When the dot-com bubble burst in the latter half of 2000, the company's market capitalization plummeted to around 10 billion yen, falling below its cash holdings of 20.7 billion yen. A divergence emerged between market valuation and intrinsic value, and in 2001 the Murakami Fund demanded cash distribution, among other pressures, forcing a reconsideration of capital policy.

On the other hand, the 20 billion yen-plus in funds served as a long-term safety net, enabling aggressive investment in ventures such as the Ameba business. While accompanied in the short term by the side effects of questions over fund deployment and stock price stagnation, the long-term securing of growth capital allowed the company to maintain a posture of continuous investment in new businesses.

| Date | Amount Raised | Estimated Valuation | Notes |

| 1999/3/18 | 0.10 hundred million yen | 0.10 hundred million yen | Company incorporation |

| 1999/3/11 | 0.20 hundred million yen | 0.30 hundred million yen | Third-party allotment |

| 1999/6/29 | 0.20 hundred million yen | 0.32 hundred million yen | Third-party allotment |

| 1999/9/22 | 0.53 hundred million yen | 1.34 hundred million yen | Third-party allotment |

| 1999/9/30 | 0.17 hundred million yen | 1.51 hundred million yen | Third-party allotment |

| 2000/3/24 | 207 hundred million yen | 624 hundred million yen | Public offering (IPO) |

- Date

- 1999/3/18

- Amount Raised

- 0.10 hundred million yen

- Estimated Valuation

- 0.10 hundred million yen

- Notes

- Company incorporation

A loss-making company raised 20.7 billion yen at a valuation of 62.4 billion yen, only to see its market cap crash to 10 billion yen six months later. The abnormal situation of cash holdings exceeding enterprise value invited intervention from the Murakami Fund. Yet ironically, the 20 billion yen-plus in cash raised at the bubble's peak enabled the long-term investments in Ameba and Abema that followed. The structure in which funds raised at the bubble's peak became the investment capacity for a decade-plus of loss-making businesses is fascinating.

Lifetime employment declaration

A 30% attrition rate—hiring 200 per year only to lose 100. To end this war of attrition, President Fujita made the un-startup-like choice of declaring 'lifetime employment.' Benefits like the Two-Station Rule and Yasunde Five were judged rational compared to recruitment costs. Placing the then-young Tetsuhito Soyama as HR Division head to redesign both systems and culture cut the attrition rate in half to 15%. The organizational stability underpinned advertising sales expansion, achieving a workforce exceeding 1,000.

BackgroundRising attrition and emergence of organizational dysfunction

Following the collapse of the dot-com bubble, CyberAgent began facing challenges in retaining mid-career hires recruited during the rapid expansion phase. By 2002, the attrition rate reached approximately 30%, creating a situation where even with 200 annual hires, approximately 100 employees were leaving. Recruitment expansion premised on growth had turned into a structure that undermined organizational stability.

Additionally, friction arose between mid-career managers in their 30s from large corporations and employees in their 20s who had been with the company since its founding, causing the chain of command to malfunction. Susumu Fujita attempted countermeasures such as gifting a portion of his own shares to employees, but these did not achieve a fundamental solution. The situation had entered a phase where redesigning the organizational culture was imperative.

DecisionLifetime employment declaration and institutional reform

In 2003, Susumu Fujita declared the introduction of a "lifetime employment system" and shifted course toward building an environment where employees could work long-term. Investment in benefits began, including a housing subsidy system (the "Two-Station Rule" providing subsidies for employees living within two train stations of the office) and the "Yasunde Five" policy granting five consecutive vacation days after two years of tenure. These were judged to be rational when compared against recruitment costs.

Furthermore, company-wide assemblies were held twice annually, fostering unity through awards and sharing. In 2005, an HR Division was newly established, and Tetsuhito Soyama was appointed as its head. The development of evaluation systems and interview frameworks was advanced, and talent retention was placed at the center of management priorities. Organizational reform was pursued on both the institutional and cultural fronts.

ResultImproved retention and strengthened growth foundation

As a result of the reforms, the attrition rate improved to approximately 15% by 2006. As talent retention progressed, the sales organization stabilized and the expansion of the advertising business accelerated. The number of employees surpassed 1,000 in fiscal 2005 and 1,400 in fiscal 2006, with the organizational scale expanding sustainably.

This reform was not merely an expansion of benefits but signified a transition from venture-style fluidity to a long-term employment organization. Improved talent retention enhanced sales capability and business continuity, and the company established the organizational foundation to support its expansion phase. The 2003 organizational reform became the turning point for management stabilization.

| Name | Year Joined | Position | Previous Company |

| Go Nakayama | 1999/8 | Head of Management Division (2003–) | Sumitomo Corporation |

| Shinichi Saijo | 2000/3 | Head of Business Strategy Office (2000–) | ITOCHU Corporation |

| Akinori Takamura | 1999/1 | Advertising Agency Business Lead | Kowa |

| Tetsuhito Soyama | 1999/4 | HR Division Head (2005–) | Isetan |

- Name

- Go Nakayama

- Year Joined

- 1999/8

- Position

- Head of Management Division (2003–)

- Previous Company

- Sumitomo Corporation

A 30% attrition rate—hiring 200 per year only to lose 100. To end this war of attrition, President Fujita made the un-startup-like choice of declaring 'lifetime employment.' Benefits like the Two-Station Rule and Yasunde Five were judged rational compared to recruitment costs. Placing the then-young Tetsuhito Soyama as HR Division head to redesign both systems and culture cut the attrition rate in half to 15%. The organizational stability underpinned advertising sales expansion, achieving a workforce exceeding 1,000.

CyberAgent ranked fourth in the 'Best Workplaces' survey conducted by Great Place to Work® Institute Japan in 2012.

However, the path was not smooth. A company whose attrition rate once exceeded 30% launched efforts to strengthen internal systems from 2003 and came to be called a great place to work. I believe the internal systems before that point had various contradictions.

The thorough pursuit of performance-based evaluation increased individual play and created a tense atmosphere. The influx of mid-career hires created conflicts between veteran employees and newcomers. New businesses often didn't work out, and when they were discontinued, there was no follow-up, resulting in excellent talent leaving the company.

Looking back now, I think the president's philosophy on HR wasn't properly communicated to the front lines during that period. The president frequently spoke about the importance of people and often mentioned it on his blog, but front-line employees—especially mid-career hires—perceived it as 'what you say and what you do are different.' I believe there was an unbridgeable gap between management and the front lines.

People say the IT industry has abundant talent, but in reality, hiring good people is extremely difficult. While the mid-career recruitment market has become more fluid than before, it's still truly hard to hire excellent people. That's precisely why I want them to grow within the company. Once we secure new graduates, we educate them while making our utmost effort to keep them from leaving.

The trigger was the mass departure of employees following the collapse of the dot-com bubble in 2000. I had also been swept up in the prevailing trends of performance-based and meritocratic management. These systems work well when the company is doing well, but once things decline, they're very fragile. Employees left in droves and the internal atmosphere deteriorated. Feeling this was unsustainable, from 2003 I introduced the lifetime employment system and transitioned to a framework for retaining employees.

(Note: On the effect of housing subsidies limited to the headquarters area) The effect is tremendous. Since many of our employees are single, a 30,000 yen housing subsidy enables people who could otherwise only afford to live in the outer suburbs of Tokyo to live near Shibuya. The primary aim is to free them from commuting stress so they can work freely. Many people want to quit because commuting is painful. Once someone changes jobs, our unique housing subsidy naturally disappears. Even if they move to a company with the same salary, they can no longer afford to live near Shibuya. We aimed for this to become a barrier to job-hopping. And it worked brilliantly.

Ameba Business Division established

The predecessor was reassigned, and President Fujita assumed direct control, declaring profitability by 2009 or resignation. The approximately 6 billion yen upfront investment was sourced from IPO proceeds. Setting monthly PV as the KPI was a decision based on the clear revenue structure of advertising inventory = PV. The transition from an advertising agency model proportional to sales headcount to a leverageable media ownership model was a structural transformation. Without this shift, the subsequent large-scale investment in Abema could not even have been conceived.

BackgroundSeeking to break free from advertising dependence

As of 2004, CyberAgent's core business was internet advertising, with revenue proportional to the number of sales personnel. It was a labor-intensive model of securing advertising inventory and advertisers, and scaling required workforce expansion. Susumu Fujita recognized the need for a leverageable business not dependent on headcount and decided to enter the media business by owning advertising inventory.

Ameba Blog, launched in 2004, rapidly expanded traffic through celebrity blogs, but concentrated traffic on popular articles caused frequent server outages during nighttime hours. A structural problem persisted where growing page views did not proportionally translate into advertising revenue, and the break-even point remained elusive. The lack of scalability surfaced as a management challenge.

DecisionRestructured under CEO's direct oversight

In July 2005, the Ameba Business Division was established, and Susumu Fujita assumed direct oversight of the restructured operation. The previous person in charge was reassigned, and the CEO made clear his posture of bearing direct accountability for results. Setting profitability by 2009 as a goal and indicating readiness to resign if the target was not met, he demonstrated the seriousness of the turnaround commitment to the organization both internally and externally.

Monthly page views were designated as the KPI, setting the metric most directly linked to advertising sales as the top priority. Approximately 6 billion yen in upfront investment was planned, and by separating the base of operations from headquarters, a standalone profit consciousness was instilled. The decision was to execute a large-scale investment within financial tolerance, using the funds secured at the time of listing.

ResultRebuilding the growth foundation

Under the CEO's direct oversight, the organization was reorganized, and infrastructure expansion and content enrichment progressed. Page views expanded incrementally, and the growth in advertising inventory drove improvements in the revenue structure. While losses continued in the short term, the presence of the media business steadily grew.

As a result, Ameba grew into the pillar symbolizing the company's transformation from an advertising-dependent enterprise to one owning its own media. The approximately 6 billion yen in upfront investment carried risk, but the funds secured at listing made the challenge possible. The 2005 establishment of the division became the turning point at which the company took its first serious step toward becoming a platform company.

The predecessor was reassigned, and President Fujita assumed direct control, declaring profitability by 2009 or resignation. The approximately 6 billion yen upfront investment was sourced from IPO proceeds. Setting monthly PV as the KPI was a decision based on the clear revenue structure of advertising inventory = PV. The transition from an advertising agency model proportional to sales headcount to a leverageable media ownership model was a structural transformation. Without this shift, the subsequent large-scale investment in Abema could not even have been conceived.

What attracted attention about so-called internet businesses during the IT bubble was the increasing-returns model, with very high profit margins and the ability to operate at low cost.

On the other hand, the advertising agency business, while the market itself is growing, tends to be labor-intensive and is not the kind of business that can deliver the results investors expected. So I thought we needed to do media, and we launched various businesses including 'cyberclick!' and 'melma!'. But they were all small-scale, and I always had a complex about not having an iconic media property like Rakuten or Yahoo.

So when blogs emerged, I felt the possibility of creating a new media property, and decided to pursue it to the end under the Ameba brand. Since I positioned Ameba Blog at the center of the company's growth strategy, we absolutely had to make it succeed.

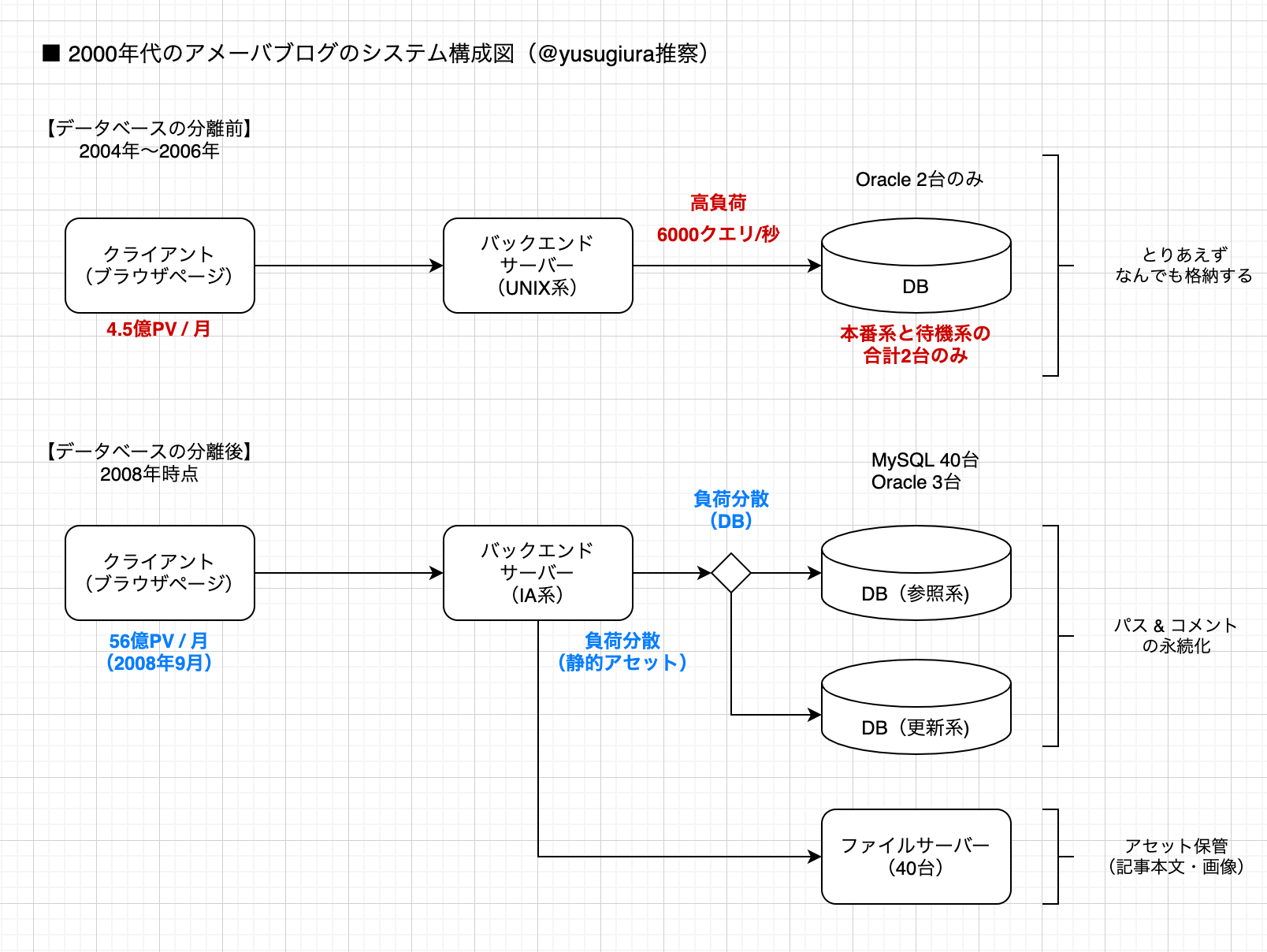

Commenced engineer recruitment

15 million daily PV, 6,000 queries per second at peak. The outsourced structure couldn't withstand this load, and nighttime server outages became routine. Fujita declared on his own blog: '20 hires by end of June.' Makoto Sato, who joined the company, spent three years rebuilding the architecture from Oracle to MySQL with load distribution, achieving profitability in the fiscal year ending September 2010. This was the turning point where a sales-driven company transformed into a technology company—without this experience, neither the subsequent gaming nor ad-tech businesses would have been possible.

BackgroundLimits of the outsourced development model exposed

Ameba Blog had grown traffic through the rapid expansion of celebrity blogs, but concentrated nighttime access caused frequent server outages. Against a load of 15 million daily page views and 6,000 queries per second at peak, the outsourcing-centered development structure was unable to make rapid improvements. Even as PV grew, advertising revenue did not scale proportionally, and technical constraints were defining the ceiling of growth.

Additionally, structural problems had emerged in the architecture—an Oracle-centric configuration, lack of Read/Write separation, and inadequate index design that did not anticipate load distribution. Modifying the database of a running service was highly difficult, and the company faced a situation where fundamental resolution was impossible without internalizing the technology.

DecisionPivoted to in-house engineering

In May 2006, Susumu Fujita announced the commencement of in-house engineer recruitment on his own blog, declaring '20 hires by the end of June.' This was a policy to internalize development capabilities and increase the speed of system improvements, breaking free from outsourcing dependence. Measures to strengthen recruitment were executed, including office renovation, compensation improvements, and CEO attendance at final interviews.

That same year, Makoto Sato joined the company and earned trust through handling first-response incident management. Over three years, he rebuilt the load-balancing architecture. The migration from Oracle to MySQL was executed, along with static asset separation and index optimization. The company pivoted toward building infrastructure capable of withstanding surging traffic.

ResultProfitability and engineering culture established

Infrastructure improvements progressed incrementally, achieving stable operations around 2009. Outages during traffic spikes were dramatically reduced, and a structure emerged where PV growth could translate into revenue. With technical constraints relaxed, expansion of advertising inventory and revenue improvement progressed simultaneously.

In the fiscal year ending September 2010, the Ameba business achieved profitability. In addition to advertising revenue, a subscription model was also established, and it grew into a high-margin business. Furthermore, the success experience of internalizing technology spread across the organization, and a culture of engineering-first became embedded. The 2006 commencement of recruitment became the starting point for the company's transformation into a technology company.

15 million daily PV, 6,000 queries per second at peak. The outsourced structure couldn't withstand this load, and nighttime server outages became routine. Fujita declared on his own blog: '20 hires by end of June.' Makoto Sato, who joined the company, spent three years rebuilding the architecture from Oracle to MySQL with load distribution, achieving profitability in the fiscal year ending September 2010. This was the turning point where a sales-driven company transformed into a technology company—without this experience, neither the subsequent gaming nor ad-tech businesses would have been possible.

Smartphone shift declared

The smartphone shift declaration coincided with the establishment of Cygames, and 'Rage of Bahamut' became a hit domestically and internationally. On the advertising side, in-house investment accelerated from AMoAd to the establishment of the Ad Technology Division. The transition from a PC-dependent advertising agency model to the twin pillars of gaming × ad tech culminated in record net income of 14.7 billion yen in fiscal 2015. The fact that a partial sale of Cygames shares subsequently yielded 6.06 billion yen, with subsidiary cultivation also contributing to capital policy, should not be overlooked.

BackgroundRecognition of the PC-centric model's limits

Around 2010, internet usage was rapidly migrating to smartphones. CyberAgent had grown centered on advertising and blogs, but the PC-based business structure faced growing likelihood of being unable to maintain medium-to-long-term competitive advantage. Susumu Fujita advocated 'CyberAgent as a technology company' and made the shift toward engineering-led operations explicit.

Simultaneously, breaking free from sole dependence on advertising was also a challenge. Rather than an advertising model that scaled proportionally with headcount, a product-driven business that scaled was needed. The spread of smartphones meant expansion of the gaming and app markets, and this was recognized as an opportunity to establish new revenue sources.

DecisionSmartphone focus and organizational restructuring

In May 2011, the smartphone shift was declared and a company-wide organizational restructuring was executed. Cygames was established as a gaming subsidiary, and development of smartphone games was launched in earnest. 'Rage of Bahamut,' released in September 2011, became a hit both domestically and internationally, ranking highly on both Google Play and the App Store.

Additionally, in the advertising space, in-house investment in ad technology commenced. Starting with 'AMoAd,' a smartphone ad network, multiple operational tools were developed, and in 2013, an Ad Technology Division was established. The company transitioned to a structure with product development and advertising technology as twin engines, reconstructing the business portfolio around smartphones.

ResultEstablishment of high-margin businesses

The results of the smartphone shift directly impacted business performance. Cygames continued to create hit titles, and the gaming business grew into a revenue pillar. In the advertising space, the expansion of programmatic advertising strengthened the revenue structure. The business portfolio pivoted from PC-dependent to smartphone-led.

As a result, record-high net income of 14.7 billion yen was achieved in fiscal 2015. The smartphone focus strategy was not mere trend-following but signified a structural transformation into a technology-led company. The 2011 declaration and organizational restructuring became the starting point for CyberAgent's transition into its second growth phase.

| Product Name | Function | Notes |

| AMoAd | Ad network | Launched in 2011 |

| CA Reward | Reward advertising | |

| Force Operation X | Solution | |

| CAMP | Ad effectiveness measurement |

- Product Name

- AMoAd

- Function

- Ad network

- Notes

- Launched in 2011

The smartphone shift declaration coincided with the establishment of Cygames, and 'Rage of Bahamut' became a hit domestically and internationally. On the advertising side, in-house investment accelerated from AMoAd to the establishment of the Ad Technology Division. The transition from a PC-dependent advertising agency model to the twin pillars of gaming × ad tech culminated in record net income of 14.7 billion yen in fiscal 2015. The fact that a partial sale of Cygames shares subsequently yielded 6.06 billion yen, with subsidiary cultivation also contributing to capital policy, should not be overlooked.

A system for not losing is already in place. The 'mechanism for continuously creating new services,' which we built through trial and error with 'Ameba,' exists within the company. When entering a new market, some companies casually draft acquisition plans saying 'just buy what we're good at,' but those usually fail. Under our policy of 'start small and grow big,' we have a solid system for creating services in-house. Outsourced development is too slow to compete. We also have thorough systems in place for handling everything from planning to development to operations in-house. At each stage of the process, excellent rules are firmly established.

The SAP business division I oversee is one of the most watched and fastest-growing domains, not just within our company but across the entire internet business landscape. (...) Cygames, which we established as a consolidated subsidiary in May 2011, developed a massive hit title domestically called 'Rage of Bahamut,' and over the past year has also succeeded in global expansion. Under the English title 'Rage of Bahamut,' it achieved the No. 1 position in overall app revenue rankings on both the US Google Play and US Apple Store. (...) More than 5 million members worldwide are enjoying the game. The achievement of 'Rage of Bahamut' proved that smartphone games originating from Japan can succeed as-is overseas.

AbemaTV established

Established as a 60:40 joint venture with TV Asahi, entering the market with a design distinct from existing video services: 18 channels of free, always-on broadcasting. Fujita explicitly declared 'we will continue investing for 10 years,' premised on annual losses of hundreds of billions of yen. By 2022, negative equity reached 111.1 billion yen, but the gaming business's high profitability continued to sustain the investment. The posture of tolerating approximately 6 billion yen in losses for Ameba and then orders-of-magnitude-larger losses for AbemaTV lies on the extension of the management style born from the capital surplus acquired through the 2000 IPO.

BackgroundPreparing for the arrival of the video era

Around 2015, the spread of smartphones and the advancement of telecommunications infrastructure were making video viewing an everyday activity. Additionally, Netflix's entry into Japan confirmed that the expansion of the online video market was irreversible. CyberAgent had built its revenue foundation on advertising and gaming, but was considering entry into the video space as the next large-scale market.

At the same time, the company lacked expertise in program production, and solo entry had its limits. Susumu Fujita engaged in extensive discussions with TV Asahi, envisioning a concept that combined the internet's technological capabilities with a broadcaster's production capabilities. A joint venture format that complemented each party's strengths became the prerequisite for entering the video market.

DecisionEstablishment of the AbemaTV joint venture

In April 2015, AbemaTV was established as a joint venture with TV Asahi, with ownership split at 60% CyberAgent and 40% TV Asahi. A framework was constructed that maintained CyberAgent's initiative while incorporating broadcast content production capabilities. In April 2016, the service launched as a free, always-on broadcast-style video streaming service.

At launch, approximately 18 channels were programmed, covering diverse genres including news and anime. The structure entailed substantial costs for program production and content procurement, and the decision was made to commit to long-term investment premised on annual losses of hundreds of billions of yen. Susumu Fujita explicitly stated the policy of continuing investment for 10 years.

ResultMassive investment and strategic positioning

AbemaTV grew its cumulative downloads and commenced advertising sales, but the cost burden was heavy and the entity fell into negative equity. By 2022, negative equity reached 111.1 billion yen, indicating a substantial financial burden. The management decision prioritized market establishment over short-term profitability.

However, the gaming business's high profitability supported the investment base, and the company continued investing from its own funds. AbemaTV built a distinctive position in online video and formed the foundation for a media vision rivaling terrestrial broadcasters. The 2015 joint venture establishment became the starting point for the company's long-term strategy of aspiring to become a next-generation media company.

| Fiscal Year | Revenue | Cost of Sales | Operating Profit | Negative Equity |

| FY2018 | 60 | 195 | -189 | 0 |

| FY2019 | n/a | n/a | n/a | 665 |

| FY2020 | 153 | 262 | -169 | 836 |

| FY2021 | 258 | 316 | -137 | 992 |

| FY2022 | 365 | 381 | 113 | 1111 |

- Fiscal Year

- FY2018

- Revenue

- 60

- Cost of Sales

- 195

- Operating Profit

- -189

- Negative Equity

- 0

| Channel Name | Category (estimated) |

| Abema News | Co-produced with TV Asahi (produced by a production subsidiary with 51% stake) |

| Variety CHANNEL | Licensed content |

| Drama CHANNEL | Licensed content |

| WORLD SPORTS | Licensed content |

| Abema PRODUCE | Licensed/produced content? |

| Fishing | Licensed content |

| Anime 24 | Licensed content |

| Mahjong | Licensed content |

| Board Sports | Licensed content |

| Retro Anime | Licensed content |

| Late-Night Anime | Licensed content |

| Documentary | Licensed content |

| Abema RADIO | Produced content? |

| Pets | Licensed content |

| CLUB CHANNEL | Licensed content |

| REALITY SHOW | Licensed content |

| Abema SPECIAL | Licensed content? |

| Ameba FRESH | Licensed content? |

- Channel Name

- Abema News

- Category (estimated)

- Co-produced with TV Asahi (produced by a production subsidiary with 51% stake)

Established as a 60:40 joint venture with TV Asahi, entering the market with a design distinct from existing video services: 18 channels of free, always-on broadcasting. Fujita explicitly declared 'we will continue investing for 10 years,' premised on annual losses of hundreds of billions of yen. By 2022, negative equity reached 111.1 billion yen, but the gaming business's high profitability continued to sustain the investment. The posture of tolerating approximately 6 billion yen in losses for Ameba and then orders-of-magnitude-larger losses for AbemaTV lies on the extension of the management style born from the capital surplus acquired through the 2000 IPO.

From the TV broadcasters' perspective, adapting to the internet and smartphones is an urgent priority, but within their corporate culture, they don't seem well-positioned to accomplish this. Nor could they find a suitable acquisition target. So I proposed that we would build it for them.

I am fully aware that we are generating large losses, but history has proven that media businesses cannot succeed or be monetized without first creating compelling content. Therefore, we view the current situation strictly as upfront investment, and believe what matters is to continuously produce good content. (...) We plan to nurture AbemaTV over a 10-year horizon into a pillar of the company. Beyond synergies with existing businesses in advertising and gaming, new businesses originating from AbemaTV will also emerge. We intend to place AbemaTV at the center of the company and pursue developments that will benefit the company over the medium to long term.